Introduction

Web3 & Blockchain Consultancy :

How to create a Cryptocurrency: Step-By-Step Guide

Cryptocurrencies are digital forms of currency that operate on blockchain technology, functioning similarly to traditional money. They enable people to buy goods or receive payments for services. The key difference is that cryptocurrencies require an online system to process and confirm transactions. Currently, there are thousands of cryptocurrencies available for trading. This vast number is possible because, unlike traditional currencies that need governmental endorsement, anyone with the necessary skills can launch a cryptocurrency. However, not all cryptocurrencies gain popularity; the ones that do typically offer both functionality and ease of use.Key Takeaways

- Ways to Create a Cryptocurrency: You can create a cryptocurrency by developing a new blockchain, modifying an existing blockchain, or using tools provided by an existing blockchain platform.

- Cost Considerations: Developing a new blockchain is typically more expensive, requiring significant resources for hardware and expertise. Using an existing blockchain platform can be more cost-effective.

- Compliance: It’s crucial to ensure your cryptocurrency project complies with the legal frameworks in your jurisdiction. This involves understanding and navigating the regulatory environment to avoid potential legal issues.

Understanding Key Elements Before Making Your Cryptocurrency

Embarking on the journey of creating your cryptocurrency is akin to developing digital property on the internet—it needs effective marketing to ensure it picks up momentum and is embraced by a community. Starting with the fundamentals: When launching a cryptocurrency, you can opt to develop either a coin or a token. Coins operate on their own dedicated blockchain, whereas tokens are built on pre-existing blockchain networks. Both types rely on blockchain technology for enhanced security and decentralized operations. There are three primary methods for creating a cryptocurrency: developing a new blockchain for your coin, modifying an existing blockchain to create a new coin, or issuing a token on an already existing blockchain. Deciding which path to take involves considering several factors including legal implications, potential use cases, tokenomics, and initial costs. The complexity of the task ahead will vary, requiring a range of skills from basic to advanced programming, significant time investment, financial resources, and robust perseverance (a mix of determination, resilience, and a touch of daring). The most formidable task, however, will be the ongoing maintenance, nurturing, and expansion of your cryptocurrency.Considerations Before Creating a Cryptocurrency

Before diving into how to make a cryptocurrency, it’s essential to weigh several key factors. While some considerations are straightforward, others, such as legal concerns, can become complex challenges without proper preparation.Legal Status in Your Jurisdiction

Initially, verify the legality of developing and operating a cryptocurrency in your region. Some nations, like China, have completely banned cryptocurrencies, whereas others heavily regulate them. Even in jurisdictions like the US, the regulatory landscape can be ambiguous and subject to sudden shifts that could affect the crypto environment negatively.Choosing the Right Consensus Mechanism

Historically, the crypto industry favored proof-of-work (PoW) mechanisms over proof-of-stake (PoS). The choice of a consensus mechanism is crucial as it influences the network’s energy consumption, level of decentralization, and security. For instance, Bitcoin operates on a PoW mechanism, known for its robust security and decentralization but criticized for high energy consumption. Conversely, Ethereum significantly reduced its energy footprint by switching from PoW to PoS in its recent Merge update.Defining the Purpose and Use Case

Every cryptocurrency should have a clear use case or purpose, which will dictate the blockchain technology and features needed. This unique selling proposition should be well-articulated in the project’s whitepaper.Deciding Between a Coin and a Token

Choosing to create a token rather than a coin can be more practical and cost-effective. Tokens can be quickly created on existing blockchains like Ethereum, utilizing their established security and ecosystem. In contrast, launching a coin requires building a new blockchain, which is more resource-intensive. Notably, many successful cryptocurrencies such as Cardano, BNB Coin, Tron, and Chainlink started as tokens on Ethereum’s network before migrating to their own blockchains.Tokenomics: A Crucial Aspect

Tokenomics is critical for understanding the supply dynamics and economic model of a cryptocurrency. This includes factors like the total supply of tokens, their distribution schedule, holdings by the creators or early investors, and mechanisms for token burn or buyback. Effective tokenomics is essential for attracting informed investors and ensuring the long-term viability of the cryptocurrency.Ways to Make a Cryptocurrency

There are several methods to create a cryptocurrency, depending on your technical expertise, budget, and desire for creative control:Develop a New Blockchain with Its Own Cryptocurrency

Creating a brand new blockchain allows you to develop a native cryptocurrency specific to that chain. This approach generally requires programming and software development capabilities, alongside a deep understanding of blockchain mechanics. Although this method may demand significant time and financial resources for setup and equipment, it offers the greatest flexibility in terms of currency design, governance, and choosing a consensus mechanism.1. Modify an Existing Blockchain

Another way to make a cryptocurrency is by forking or altering the source code of an existing blockchain, thus creating a new separate blockchain. This method involves using the existing codebase as a foundation and customizing it to suit your requirements, resulting in a unique blockchain and cryptocurrency. This is particularly accessible if the original blockchain code is open-source, as it lowers the barriers for those with limited coding skills or resources.Launch a Cryptocurrency on a Pre-existing Blockchain

For those looking for a straightforward approach with minimal coding, launching a new cryptocurrency on an established blockchain might be ideal. Platforms like Ethereum and BNB Chain offer the capability to create non-native tokens. These tokens operate on the blockchain’s infrastructure but are not integral to the blockchain itself.How to Create a Cryptocurrency, Step-by-Step

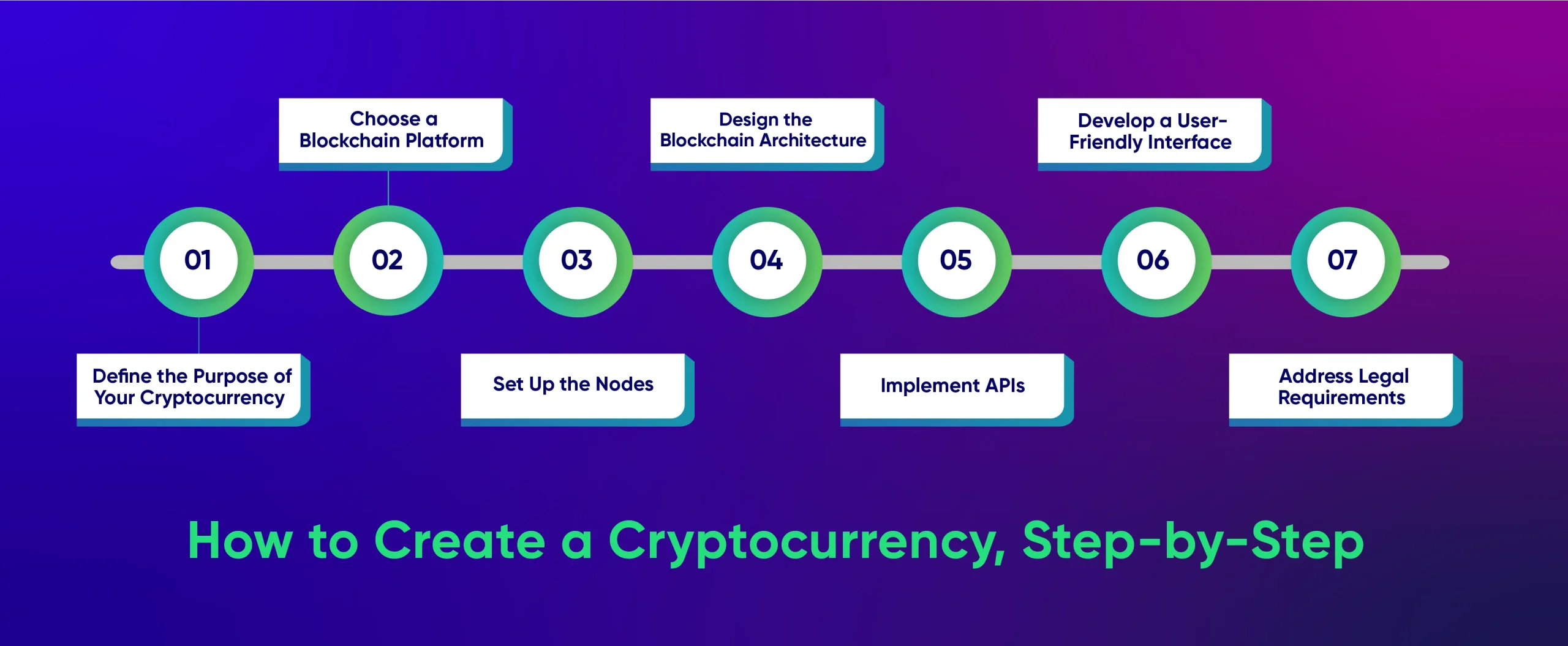

Here’s a guide on how to create a cryptocurrency, detailing the considerations during development and the sequential steps involved in the creation process:

1. Define the Purpose of Your Cryptocurrency

The initial step in creating a cryptocurrency is fundamental yet critical: Creators must identify a compelling purpose for their digital currency. Like traditional money, cryptocurrencies can fulfill various roles:- Money Transfer

- Alternative store of wealth

- Support for smart contracts

- Verification of data

- Management of smart assets

2. Choose a Blockchain Platform

The foundation of any cryptocurrency is its blockchain, which records and verifies every transaction across a decentralized network, thus ensuring security and transparency. The core of the blockchain is its consensus mechanism, which validates transactions and prevents fraud. Different consensus mechanisms include:- Proof of Work (PoW): Miners solve complex computations to form a block and receive cryptocurrency as a reward.

- Proof of Stake (PoS): Coin owners validate block transactions based on the number of coins they hold and stake.

- Delegated Proof of Stake (DPoS): Coin holders vote for certain validators who are responsible for securing new blocks.

- Proof of Elapsed Time (PoET): Rewards are given to participants based on how long they have been participating in the network.

3. Set Up the Nodes

Nodes are crucial as they process transactions and maintain the integrity of the blockchain. Considerations when setting up nodes include:- Access control to the nodes (public vs. private)

- Node hosting solutions (cloud vs. local hosting)

- Choice of operating system, with preferences often given to open-source systems like Ubuntu or Fedora for flexibility

- Hardware requirements to ensure efficient processing of transactions

4. Design the Blockchain Architecture

Blockchain architecture can vary significantly in how it manages data exchanges:- Centralized: A primary node receives data from numerous nodes.

- Decentralized: Nodes distribute data among themselves without a central point.

- Distributed: Nodes hold copies of the ledger, which can be either public or private depending on the setup.

5. Implement APIs

APIs (Application Programming Interfaces) connect the blockchain with other software applications, facilitating tasks like trading, data security, and analytics. Developers may need to integrate existing blockchain APIs like Bitcore or Factom or develop custom APIs to meet the specific needs of their cryptocurrency.6. Develop a User-Friendly Interface

To ensure that users and miners can easily interact with the cryptocurrency, a robust and intuitive interface (UI/UX) is essential. This includes designing websites or applications that allow users to manage their transactions and settings effectively.7. Address Legal Requirements

Before launching a cryptocurrency, it’s important to understand and comply with legal regulations:- Establish a legal entity, such as an LLC or Corporation.

- Obtain necessary licensing from local authorities.

- Register with organizations like the Financial Crimes Enforcement Network (FinCEN) in the U.S. to prevent financial crimes.